This article was originally published in Agenda Digitale on July 27, 2026 (in Italian only).

AI models have never been more powerful. Yet, according to McKinsey, nearly two-thirds of organizations that have adopted them have failed to move AI beyond the pilot phase. The paradox is architectural. Having the world’s fastest race car is useless without fuel, without a track, and without a driver who knows how to steer without hitting a wall. And in the enterprise context, there are plenty of obstacles: the complexity of existing systems, the sensitivity of proprietary data, the rigidity of internal workflows.

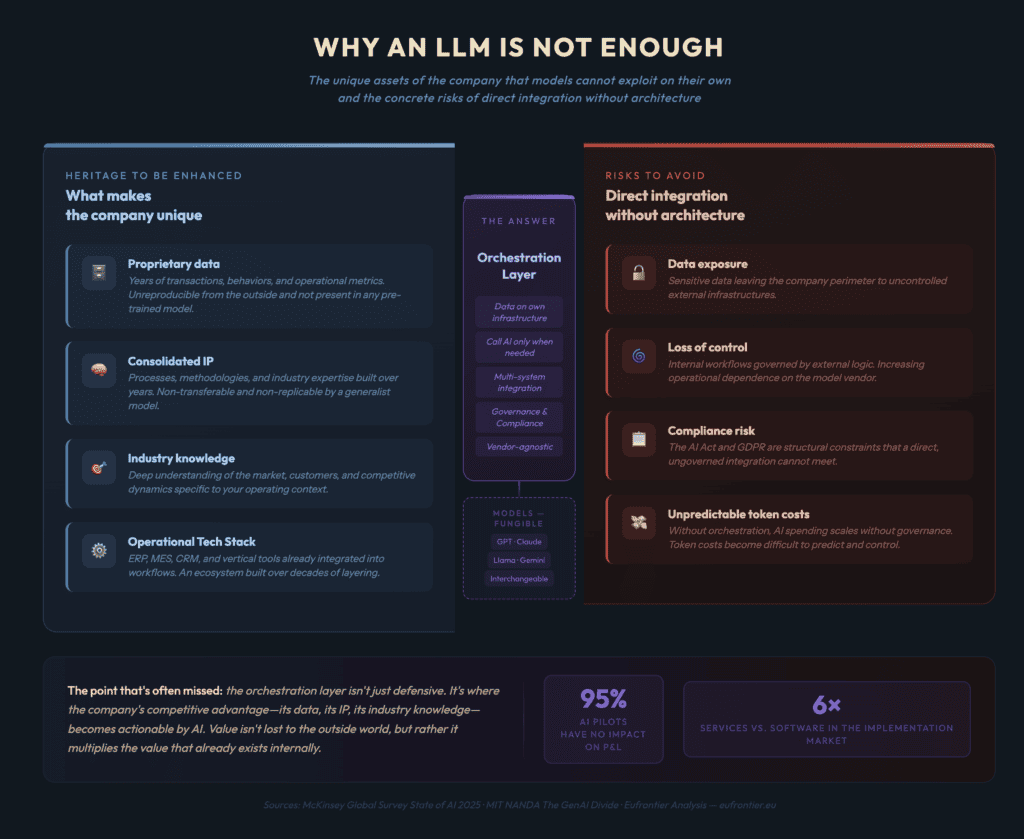

The McKinsey Global Survey State of AI 2025, conducted across nearly 2,000 organizations in 105 countries, finds that 88% of companies use AI in at least one function, but only one third has truly begun to scale the technology within the organization. The majority is stuck in what analysts call “pilot purgatory”: isolated experiments that never escape the boundaries of the proof-of-concept project. The MIT NANDA report The GenAI Divide, based on the analysis of 300 public deployments, estimates that 95% of enterprise pilots produce no measurable impact on the income statement. The problem lies not in the quality of the models, but in the way they are grafted into companies: without a dedicated architecture, they fail to leverage the unique characteristics of the context in which they are applied.

A company with years of history carries something no model possesses: proprietary data, consolidated IP, deep knowledge of its own sector, and an operational tech stack already in place. This is the asset that the mere adoption of an LLM cannot fully exploit. Connecting a model to one’s own systems without a dedicated architecture means exposing sensitive data, losing control over internal workflows, and accumulating hard-to-predict token costs. Above all, it means ceding to the outside the most valuable part of what the company knows how to do. Added to this is growing exposure to compliance risks: the AI Act and GDPR are structural constraints that a direct, ungoverned integration is unable to respect.

The market has already identified the problem. In May 2026, OpenAI launched the OpenAI Deployment Company — a fundraise of over 4 billion dollars from 19 investors including TPG, Bain Capital, and McKinsey — simultaneously acquiring Tomoro, a British AI consultancy with 150 engineers specializing in enterprise AI adoption. Almost simultaneously, Anthropic announced a joint venture with Blackstone, Goldman Sachs, and Hellman & Friedman to bring Claude into the core operations of mid-market companies, with approximately 1.5 billion dollars committed. The operating model of both initiatives is explicitly inspired by Palantir: “forward deployed” engineers who physically enter client organizations to build integration from the inside. The diagnosis is correct; the proposed therapy, however, serves interests different from those of the client company. The financial context is relevant for understanding the motive: for every euro generated in software, the market historically produces six in implementation and consulting services. This is a space the labs are trying to occupy, not out of vocation, but out of revenue necessity at a stage when valuations require demonstrating real adoption.

Vendor-specific forward deployment carries a structural limitation that Gartner analysts have already flagged: the model vendor has no visibility into the overall architecture of the client enterprise. An enterprise organization does not live in a mono-vendor ecosystem. It coexists with SAP, Salesforce, vertical industry tools, and heterogeneous databases built up over decades of technological layering. Whoever arrives to implement a single model knows their own product, not the architecture it must integrate with. The concrete risk is building an efficient AI island that does not communicate with the rest, or worse, communicates poorly. Consider a typical case in manufacturing: a demand forecasting model trained on aggregated historical data produces technically accurate forecasts, but cannot see real-time production capacity constraints, machine downtime, or batches in progress within the MES. The result is a forecast that looks brilliant on paper but is unusable in operational decisions. To this technical limitation is added a double conflict of interest: the model vendor has an incentive to maximize consumption of its own product; the co-investing private equity fund has an incentive to promote the adoption of that specific model in its portfolio companies, regardless of the quality of the solution relative to market alternatives. For a deeper look at how these agreements were structured and their financial mechanisms, I refer to the analysis published on Eufrontier: Anthropic and OpenAI bet on private equity as an enterprise distribution channel.

The answer is to build an orchestration logic that governs the use of models in the interest of the enterprise. An architecture of this kind keeps context data queryable on local or private cloud infrastructure, calls models only when the task truly requires it, integrates existing software systems, and designs AI-native workflows that respect the organization’s security and compliance rules. In this schema, the language model becomes an interchangeable tool: the competitive advantage does not lie in the model chosen today, but in the architecture the company controls and can update or replace without losing what it has built. The point that is often missed is that this architecture is not merely defensive. It is the place where the company’s competitive advantage — its data, its IP, its sector knowledge — becomes actionable by AI. Value is not ceded outward, but rather the value that already exists internally is multiplied. Building this architecture is not just a technical choice, but above all a decision about who holds sovereignty over the processes and data that make the company unique.

Who builds this layer? Not the model vendor, for the reasons already described. Not the traditional system integrator, who knows enterprise architecture but has not yet developed sufficient AI competence to design complex orchestration. The space is being occupied by an emerging category of players: companies with native AI expertise, multi-system integration capability, and a vendor-agnostic approach, who do not sell a model but an architecture for making AI work. Their competitive advantage is not strictly technological; it lies rather in the ability to read the client’s existing architecture, identify where AI produces real value, and build a layer that connects without exposing to risks. This is a role that did not exist five years ago and that the market is beginning to recognize as distinct from both the major AI players and the large traditional consulting firms.

For smaller organizations, the custom orchestration layer remains out of reach in terms of complexity and cost. The market is responding with pre-packaged solutions — such as Anthropic’s Claude for Work, which comes with native integrations for Google Workspace, Microsoft 365, and the main SaaS tools — lowering the adoption barrier at the cost of reduced customization. In this schema, the language model is a fungible tool: QuickBooks or HubSpot can replace Claude with GPT or Gemini if pricing or performance changes. The competitive advantage does not belong to the model, but to whoever owns the client relationship and the industry data accumulated over years of use. This is an acceptable trade-off for those without proprietary information assets to protect at that level of granularity; for large organizations, relying on vendor-built solutions is equivalent to outsourcing the most strategic part of their digital transformation. For a detailed analysis of how this schema plays out in small businesses through vertical software, I refer to: Vertical software: the Trojan horse of AI.

The movement of major players toward forward deployment is confirmation that the AI adoption market is still trying to stabilize. It has not yet found its footing. The major operators bring the model but not the neutrality. Traditional consultants bring knowledge of the architecture but not AI competence. In between, a precise space is opening up for those who can do both in the interest of the client. The companies that occupy it first will have an advantage that is difficult to erode — not because they use the best technology, but because they offer clients a solution that can be adopted without compromising sovereignty over their knowledge assets.