This article was originally published on MIT Technology Review on May 26th, 2026 – italian only

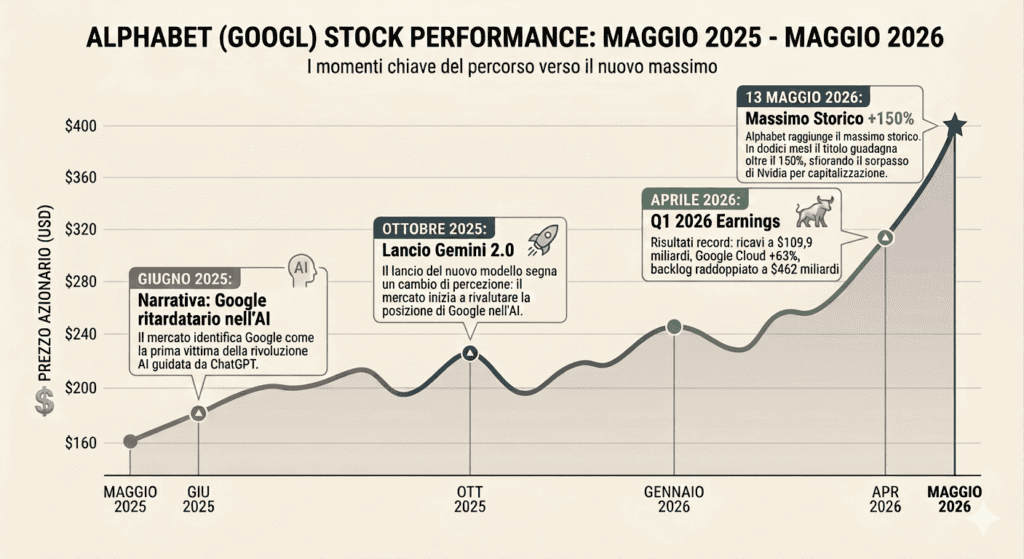

A year ago, the market narrative around Alphabet was that it was losing the new AI battle. While ChatGPT was redefining expectations for the future of online search, the market viewed Google as the first major casualty of the new technological revolution. In the first half of May 2026, the stock reached an all-time high; over twelve months it gained more than 150%, briefly surpassed Nvidia in market capitalization during after-hours trading, and became the second most valuable company in the world. The numbers made the strength of the company’s strategy impossible to ignore.

The results for the first quarter of 2026 speak for themselves: consolidated revenue grew 22% to $109.9 billion, while net income reached $62.6 billion (including $28.7 billion in financial gains), up 81% year-over-year. Google Cloud surpassed the $20 billion quarterly revenue threshold for the first time, posting 63% growth that outpaced both Azure and AWS (which grew 35% and 17% respectively during the same period), nearly doubling its backlog and more than doubling segment operating income.

Image processed by the author using Gemini Nano Banana.

The narrative portraying Google as an AI laggard has been completely disproven by real-world usage data for its LLM, Gemini. According to SimilarWeb data, within a year the model grew from 6% to 22% of global AI traffic. Gemini APIs now process 16 billion tokens per minute, up from 10 billion the previous quarter. On the enterprise side, generative AI-based products recorded 800% year-over-year growth, while paying monthly active users of Gemini Enterprise increased 40% over the last quarter. These figures cannot be explained solely by Android’s captive distribution; they indicate that the product performs well even in contexts where users are free to choose alternatives.

Although the reported figures do not yet fully reflect it, it is evident that Google’s advertising model is under pressure due to the rapid rise of generative search, which structurally compresses CTRs without reducing query volume. Management claims that AI Overviews are already monetizing at rates comparable to traditional search, and quarterly results appear to support this: Search revenue grew 19% despite the heavy integration of AI into interfaces. However, the long-term sustainability of ARPU remains an open question and can be considered the highest-impact risk for a company whose financial engine is still largely driven by online advertising.

Image processed by the author using Gemini Nano Banana.

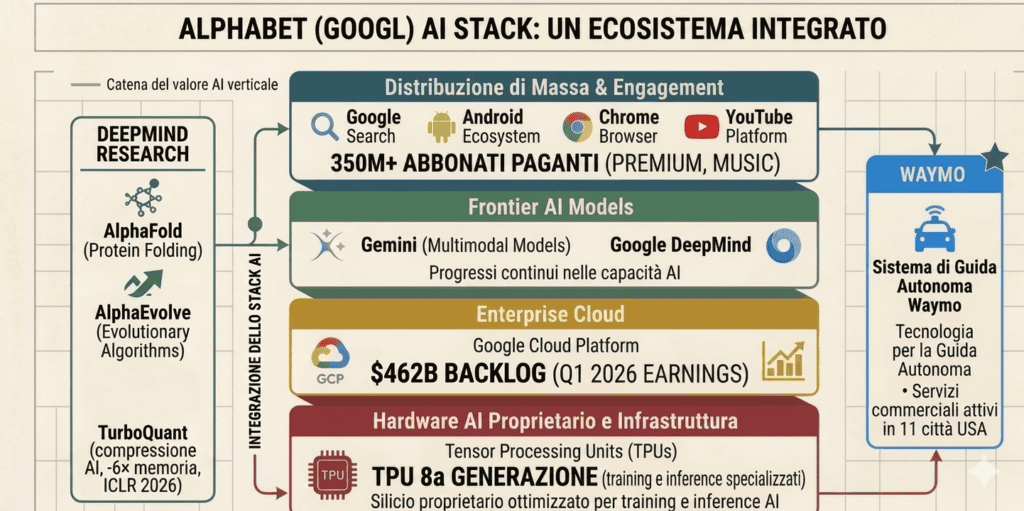

The results described above are the direct consequence of an architecture built in layers, where each layer reinforces the next. Today, Alphabet is the only company in the world that organically controls every layer of the AI value chain. Proprietary silicon through TPUs, frontier models with Gemini developed by Google DeepMind, massive-scale distribution through Search, Android, Chrome, and YouTube, enterprise cloud infrastructure, and direct consumer access through 350 million paying subscribers. No competitor possesses the same architecture, and this distinctive element is likely the deepest reason investors are choosing the company: it is not a bet on a single product, but structural exposure to the entire AI landscape.

Added to this is an element absent from any balance sheet, yet probably the most valuable asset in the entire stack: Google DeepMind. We are not simply talking about the “factory” behind Gemini, but arguably the world’s most productive applied AI research laboratory. A few examples: AlphaFold solved the protein-folding problem that molecular biology had pursued for fifty years; AlphaGeometry demonstrated Olympic-level mathematical reasoning; AlphaEvolve, announced in 2025, generated algorithms more efficient than those designed by humans across seventy years of theoretical computer science. This is not an asset that can be purchased on the market—it is built over decades, and it produces competitive returns on time horizons far beyond quarterly reporting cycles.

At the opposite end of the spectrum lies an example of where this research can lead: Waymo, Alphabet’s subsidiary and currently the world’s only operator with a commercially scaled autonomous driving service across eleven U.S. cities, delivering more than 500,000 driverless rides per week. It does not rely on external models, does not purchase cloud infrastructure from third parties, and requires no partnerships for distribution. It is vertically integrated AI in its purest form, and at this moment it has no direct operational competitor at comparable scale. Despite this, Waymo is still considered by many as a residual component of the Group’s valuation.

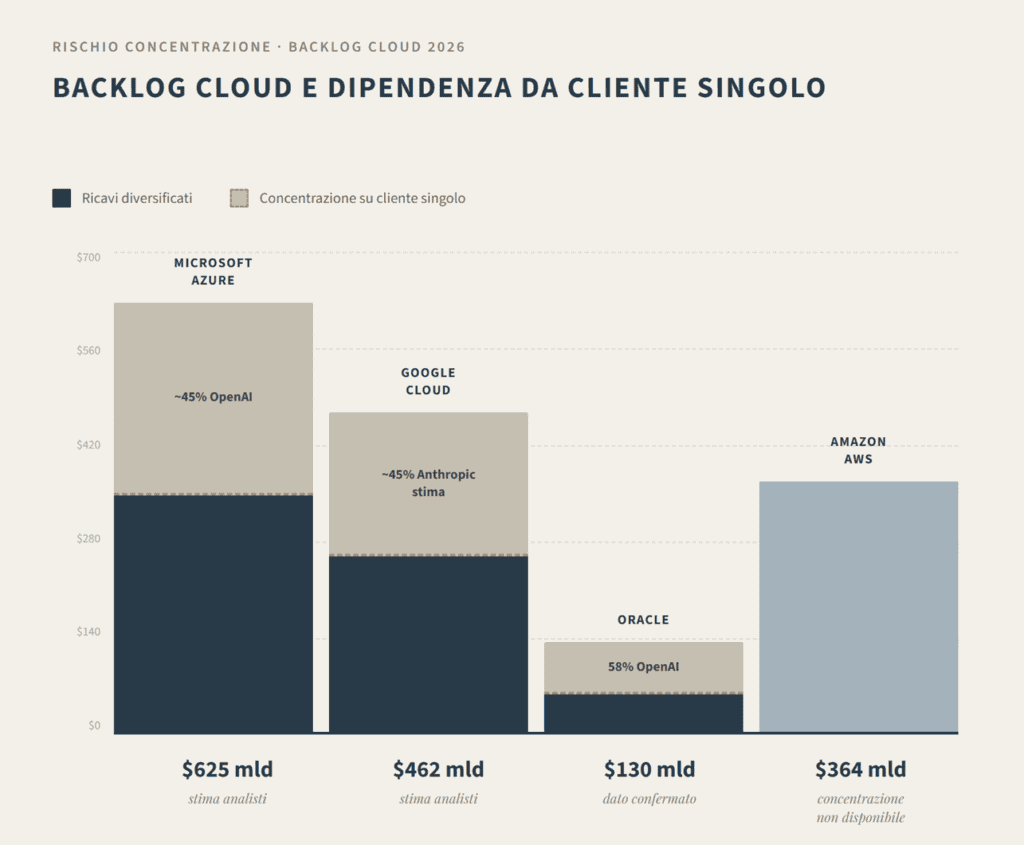

Another central strategic pillar is Alphabet’s investment commitment of up to $40 billion in Anthropic, Gemini’s primary competitor in the enterprise AI segment. This move should not be interpreted as a strategic contradiction, but rather as deliberate hedging: if the frontier-model layer converges toward commoditization, Alphabet could still maintain a key position among the major contenders by supplying infrastructure to both sides. At the same time, Anthropic itself has committed to spending approximately $200 billion on Google Cloud over the next five years—a figure which, according to some estimates, could account for nearly half of Google Cloud’s total $462 billion backlog. One can already identify a circular dynamic familiar within the tech industry: Google finances Anthropic, Anthropic purchases compute from Google Cloud, and that spending feeds the backlog that markets reward as a signal of organic demand. Oracle already paid a heavy stock-market price once it became public that a large portion of its backlog came from a single client, OpenAI. Alphabet’s situation is different, but the risk profile remains and should not be underestimated.

Image processed by the author using Claude.

To understand the significance of this strategy, it is useful to compare Alphabet with Microsoft, historically regarded as the most diversified—and therefore most defensive—Big Tech company from an investor perspective. Three balanced revenue streams (enterprise productivity, cloud, and gaming) traditionally made it structurally less exposed than Google to advertising cycles. In the AI era, however, this logic has reversed. Microsoft built its AI strategy by outsourcing the LLM layer to an external supplier, OpenAI, in which it invested approximately $13 billion. The result is that OpenAI now represents, according to estimates by several analysts, a highly significant portion (more than 40%) of the $625 billion in Remaining Performance Obligations disclosed by Microsoft during its February 2026 earnings call. This concentration exposes the company to a dependency risk absent from its traditional model. Copilot, Microsoft’s flagship AI product, saw its U.S. market share decline from 18.8% to 11.5% in six months. In September 2025, Microsoft was forced to integrate Anthropic’s Claude into Microsoft 365, choosing a model that runs on competitor AWS rather than Azure—a sign that its in-house solution was insufficient to meet market expectations. While Microsoft’s horizontal diversification turned into vertical dependence on an external provider, Alphabet’s vertical concentration became a source of strategic autonomy. In the AI paradigm, building everything internally has proven more defensive than diversifying.

However, the most strategically significant move concerns proprietary chips (“TPUs”). Alphabet developed its TPUs as internal infrastructure, with the goal of reducing cost per query and preserving margins on workloads requiring enormous computational resources. The promises have been delivered: with the seventh generation (“Ironwood”), performance improved fourfold compared to the previous generation, while the eighth generation (“TPU 8i”) delivers 80% more performance at the same cost relative to Ironwood. Then came the turning point: an agreement with Meta for TPU access, the first signal that this internal infrastructure is becoming a commercial product for third parties. Current estimates project billions of dollars in short-term revenue; assuming conservatively just 5% of NVIDIA’s 2025 GPU market—estimated at $115 billion—we are talking about roughly $5 billion annually. Although the shift toward proprietary silicon is real, it will take time to operationalize at scale. Ironwood has only recently entered large-scale production, and customer adoption in cloud environments remains at an early stage. Meanwhile, Alphabet continues purchasing NVIDIA GPUs in significant quantities. The competitive advantage of proprietary silicon is structurally solid, but independence from the chip market should be viewed as a medium-term objective rather than an already achieved reality.

Alphabet’s investment plan for 2026 is set between $180 and $190 billion, with 2027 spending already described as “significantly higher.” At this scale, capex no longer measures operational necessity; it reflects conviction in the ability to convert infrastructure into revenue. Companies invest at this speed because demand exceeds available capacity, not because they are making speculative bets in uncertain environments. Still, the question that every infrastructure cycle in history eventually raises remains open: what will the return on invested capital be? History—from the fiber-optic boom of the 1990s to the cloud-computing expansion of the last decade—shows that periods where demand exceeds supply eventually reverse, and excess capacity compresses margins even for dominant players. During the April 29, 2026 earnings call, Sundar Pichai stated that Alphabet is currently “compute constrained,” meaning demand exceeds available capacity—the ideal condition for justifying spending. But historically, this is also the condition most associated with overbuilding when multiple operators invest simultaneously at similar scale. AWS, Azure, Oracle, and Google Cloud are all spending record amounts over the same period, and the risk of building excess infrastructure is real. On the other hand, unlike players such as Oracle, Alphabet is not burning cash to sustain this investment level. Operating cash flow in Q1 2026 reached $45.8 billion, exceeding capex for the same quarter, which stood at $35.7 billion. In other words, Alphabet is fully financing its AI infrastructure through internally generated cash flow, even while increasing debt issuance to optimize its financial structure.

Within the architecture described so far, there is also a significant structural risk: the vertical integration that markets reward—from chips to models to mass distribution through Search and Android—is precisely what is currently under antitrust scrutiny by both the U.S. Department of Justice and the European Commission. The search monopoly case launched by the DOJ in 2023 is now in an advanced phase: an unfavorable ruling could force Google to open its search distribution to competitors, removing the primary user-acquisition channel for Gemini and the broader AI product ecosystem. In Europe, investigations under the Digital Markets Act focus specifically on the bundling of Android, Chrome, and Google services. There is a real possibility that American or European courts could dismantle, through regulatory intervention, the very distribution architecture that today represents Alphabet’s hardest-to-replicate competitive advantage. Investors in the company are effectively betting that this vertical integration can survive regulatory scrutiny largely intact.

Alphabet’s trajectory during the AI cycle contains a broader lesson about market time horizons during technological paradigm shifts. Building vertically integrated AI—from chips to models to distribution—is a process that takes years and produces no visible advantage until the pieces connect. Markets only priced in this integration once the numbers made clear that the strategic architecture was working. The +150% gain over twelve months was not a surprise, but a delayed interpretation.

The most interesting point, however, is not what the market has already recognized. It is what it likely still has not fully seen: Waymo still valued as a residual asset, TPUs only at the beginning of their life as commercial products, DeepMind with a research pipeline whose economic effects will mature over five- or ten-year horizons, and algorithmic research such as TurboQuant that could structurally reduce model compute costs before the chip cycle has even fully been priced in. The market rewarded what it could already see; who knows what competitive advantage is still being built while attention is focused elsewhere.

Giuseppe Venezia is Head of Corporate Development at Datrix Group and has developed his professional career by applying financial expertise to the technology sector.